The banking landscape is undergoing a revolutionary transformation where convenience is king, and time is of the essence. Omnichannel banking enchanting force reshaping the way we interact with our finances.

According to Capgemini, 76% of customers expect an omnichannel experience and 59% of customers expect on-demand, anywhere anytime customer service. It isn’t just about the convenience of mobile apps; it’s about creating a cohesive ecosystem where customers can seamlessly switch between various channels.

Are you ready to dive into the world where banking meets brilliance? Let’s navigate the landscape of omnichannel banking and discover the future of financial services together!

What is Omnichannel Banking?

Omnichannel banking is a comprehensive approach to providing automated and integrated banking services across multiple channels, both physical and digital. It aims to create a cohesive and consistent experience for customers. Resultantly, customer can interact with their bank effortlessly through various touchpoints such as online platforms, mobile apps, ATMs, call centers, and physical branches.

In an omnichannel banking environment, customers can initiate transactions on one channel and seamlessly transition to another without any disruption. For example, a customer might start a transaction on a mobile app, continue it on a computer, and finalize it in a physical branch. They can complete all without losing any information or experiencing inconsistencies in the process.

Moreover, omnichannel banking includes a unified customer profile that is accessible across channels, consistent branding, and messaging. The integration of technologies like data analytics and artificial intelligence (AI) to personalize and enhance the overall customer experience.

It is driven by the desire to meet the evolving expectations of modern customers who demand flexibility, convenience, and a personalized approach to their banking interactions. This approach not only benefits customers by providing a seamless experience. Also, it helps banks to optimize their operations, improve customer satisfaction, and stay competitive in the rapidly evolving financial landscape.

Benefits of Omnichannel Banking

In omnichannel banking, customers can interact with their bank across multiple channels such as mobile banking, online banking, ATMs, branches, and more. Here are some key benefits of omnichannel for banks and customers:

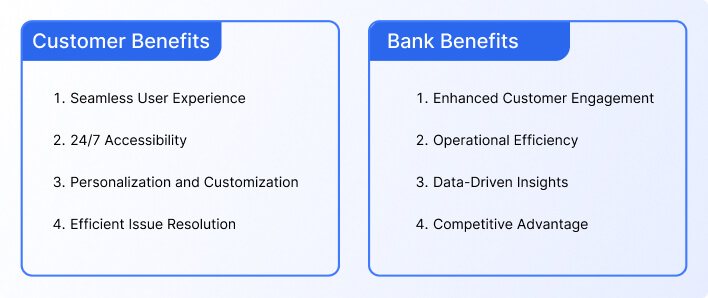

Customer Benefits

1. Seamless User Experience

When you switch from multichannel to omnichannel banking, you ensure a frictionless experience for customers by providing a consistent and unified journey across various channels. Whether accessing accounts through a mobile app, online platform, or visiting a physical branch, customers encounter a seamless transition without disruptions.

This leads to increased customer satisfaction as users can effortlessly navigate and complete transactions.

2. 24/7 Accessibility

With omnichannel banking, customers gain round-the-clock access to banking services. Whether checking account balances, transferring funds, or making payments. Most importantly, users can perform transactions at any time through online platforms or mobile apps.

This enhanced accessibility caters to the modern lifestyle. It offers convenience and flexibility to customers who may not adhere to traditional banking hours.

3. Personalization and Customization

Omnichannel financial services leverages data analytics to understand customer preferences, behaviors, and needs. This enables banks to provide personalized services and offers tailored to individual users.

It can personalize product recommendations to targeted promotional messages and customers experience a banking environment that caters specifically to their financial goals and interests.

4. Efficient Issue Resolution

In an omnichannel setup, customer issues, and inquiries can be efficiently addressed across various touchpoints. Whether through online chat, phone support, or in-person at a branch, banks can seamlessly access customer information to resolve issues promptly.

This efficiency in issue resolution contributes to a positive customer experience and fosters trust in the bank’s service capabilities.

Bank Benefits

1. Enhanced Customer Engagement

Omnichannel banking enhances customer engagement by facilitating interactions through multiple channels. Banks can engage customers through personalized communications, targeted marketing campaigns, and feedback collection.

The ability to connect with customers across various touchpoints strengthens the overall relationship and encourages customers to explore additional services.

2. Operational Efficiency

Banks can achieve operational efficiency by integrating systems and processes across different channels. Reducing redundancies and streamlining workflows contribute to a more cost-effective and resource-efficient operation.

This allows banks to allocate resources strategically. Ultimately, it improves the bottom line and ensures a sustainable and competitive business model.

3. Data-Driven Insights

Omnichannel banking platform plays an imperative role in generating valuable data on customer behavior, preferences, and transaction patterns. Analyzing this data provides banks with actionable insights into market trends, customer needs, and areas for improvement.

This data-driven decision-making empowers banks to optimize their services, design targeted marketing strategies, and stay ahead in a dynamic financial landscape.

4. Competitive Advantage

Adopting an omnichannel approach gives banks a competitive edge in the market. As customers increasingly seek seamless, personalized experiences, banks can deliver on these expectations stand out.

A comprehensive omnichannel strategy positions a bank as innovative and customer-centric to attract new customers and retain existing ones in a highly competitive industry.

Importance of Omnichannel in Retail Banking

Retail banks always need to stay relevant, competitive, and responsive to the evolving expectations of today’s digital-savvy consumers. Let’s take a look at some key reasons:

1. Enhanced Customer Experience

In retail banking, delivering an enhanced customer experience is paramount. Omnichannel financial services ensure that customers enjoy a seamless and consistent journey across various touchpoints. Whether accessing services through online platforms, or in-person at branches.

This unified experience contributes to higher customer satisfaction as users can effortlessly navigate through channels without encountering disruptions or inconsistencies.

It goes beyond mere transactions and aims to create a positive and memorable interaction at every stage of the customer’s journey.

2. Improved Customer Engagement

The omnichannel banking platform provides multiple avenues for interaction. Retail banks can connect with customers through personalized communications, targeted marketing, and feedback mechanisms. The omnichannel approach enables banks to build stronger relationships with their customers.

This heightened engagement translates to increased customer loyalty, as individuals feel more connected to the bank and are more likely to explore additional services.

3. Efficient Operational Processes

It is needless to say operational efficiency is a key advantage of adopting omnichannel strategies in retail banking. Banks can reduce redundancies and streamline workflows by integrating systems and processes across different channels.

This optimization leads to a more cost-effective and resource-efficient operation for strategic allocation of resources. And, efficient processes contribute to quicker service delivery, faster issue resolution, and an overall improvement in the bank’s ability to meet customer needs promptly.

4. Competitive Edge in the Market

In fiercely competitive retail banking, having a comprehensive omnichannel strategy provides a distinct competitive edge. Customers increasingly seek seamless, personalized experiences, and banks that deliver on these expectations stand out in the market.

A retail bank with an effective omnichannel approach is perceived as innovative, customer-centric, and forward-thinking. This competitive advantage not only attracts new customers. Also, it enhances the retention of existing ones to reinforce the bank’s position in the dynamic and evolving market.

Multichannel Vs Omnichannel Banking

Multichannel and omnichannel banking represent two distinct approaches to providing banking services across various channels.

Let’s take a closer look at the key differences between these two strategies:

Multichannel Banking

- Channel Isolation: Each channel operates independently. Online banking, mobile apps, and physical branches often function as separate entities, with limited integration.

- Siloed Customer Experience: Customers may experience inconsistencies when transitioning between channels. Information is not always shared seamlessly which is leading to a fragmented and siloed customer experience.

- Limited Cross-Channel Interaction: Customers may need to restart transactions when switching from one channel to another. For some customers it causes inconvenience.

- Channel-Specific Focus: Each channel is designed to cater to a specific set of services. For instance, online platforms may focus on transactions, while physical branches handle complex services.

- Operational Independence: Operational processes for each channel are often independent. This can result in redundancies and inefficiencies, as information is not consistently shared across channels.

Omnichannel Banking

- Unified Customer Experience: With omnichannel banking, customers can transit between channels without disruptions, as information is shared consistently.

- Consistent Branding and Messaging: Branding, messaging, and services are consistent across various channels. This creates a cohesive brand identity and reinforces the same level of service, regardless of the chosen channel.

- Cross-Channel Integration: Omnichannel banking emphasizes the integration of channels for a continuous and interconnected customer journey. Transactions can be initiated in one channel and completed in another without starting over.

- Holistic Customer View: This enables banks to offer personalized services and targeted marketing across all channels.

- Operational Harmony: Omnichannel banking platform allows for smoother workflows and optimized resource utilization by eliminating silos and redundancies.

How to Select an Omnichannel Banking Solution?

Choosing the right omnichannel banking solution is a critical decision for financial institutions, as it can significantly impact customer experience, operational efficiency, and overall business success.

Here are some key steps to consider when choosing an omnichannel banking solution:

1. Omnichannel Customer Experience Evaluation

Before selecting an omnichannel banking solution, conduct a thorough evaluation of the omnichannel customer experience it promises to deliver. Assess how well the solution integrates and streamlines customer interactions across various channels such as online platforms, mobile apps, and physical branches.

You should always look for features that ensure a seamless transition between channels, consistent branding, and personalized experiences for customers. An effective solution should prioritize enhancing the overall journey of the end-users.

2. Banking Technology Landscape Exploration

It is imperative to explore the banking technology landscape to understand the compatibility and alignment of omnichannel financial services with industry trends and emerging technologies.

When you’re planning to select an omnichannel solution you need to ensure that the solution is built on robust and scalable technology. And. it is capable of accommodating future innovations. You can examine how the solution adapts to changes in technology, security standards, and regulatory requirements for long-term success.

3. Risk Tolerance and Cost Framework Establishment

Define your organization’s risk tolerance and establish a transparent cost framework before selecting an omnichannel banking solution. Also, consider potential risks associated with implementation, such as disruptions in services or data security concerns.

Assess the total cost of ownership, including initial setup costs, ongoing maintenance expenses, and any hidden fees. Align the solution’s features and pricing structure with your risk appetite and budget constraints to ensure a financially viable and secure investment.

4. Potential Suppliers and Service Providers Assessment

Evaluate potential suppliers and service providers offering the omnichannel banking solution. Consider factors such as vendor reputation, reliability, and scalability. Assess their track record in delivering similar solutions and their ability to provide ongoing support and updates.

Look for references and case studies to validate their success stories. This comprehensive assessment helps in selecting a vendor that aligns with your organization’s goals and values.

5. Strategic Planning for Seamless Implementation

Plan strategically for the seamless implementation of the chosen omnichannel banking platform. Outline a detailed implementation roadmap that covers key aspects like user training, change management, and contingency planning.

Consider how the solution integrates with your existing systems and processes, minimizing disruptions during the transition. Define clear milestones, allocate resources effectively, and establish a communication plan to keep all stakeholders informed throughout the implementation process.

Challenges of Omnichannel Banking

While omnichannel banking offers numerous benefits, it also comes with its fair share of challenges. Some of the key challenges include:

1. Integration Complexity

Achieving seamless integration across various channels, such as online banking, mobile apps, and physical branches, poses a significant challenge. Connecting diverse systems and ensuring a unified customer experience can be complex and resource-intensive.

2. Data Security Concerns

It involves the exchange of sensitive customer data across multiple platforms. Ensuring robust security measures to protect against cyber threats and unauthorized access becomes a critical challenge in maintaining trust and compliance.

3. Consistent User Experience

Providing a consistent and cohesive user experience across different channels is a challenge. Users expect a unified journey, and discrepancies in service, features, or interface design can lead to frustration and dissatisfaction.

4. Regulatory Compliance

The banking industry is heavily regulated, and ensuring compliance with various financial regulations across different channels can be demanding. Staying abreast of evolving regulatory requirements and adapting omnichannel strategies accordingly is an ongoing challenge.

5. Technology Adoption Hurdles

The rapid evolution of technology introduces challenges related to the adoption and adaptation of new tools and platforms. Banks must invest in cutting-edge technologies while ensuring that staff and customers can seamlessly embrace and utilize these advancements.

Present and Future Omnichannel Banking Trends

Omnichannel banking trends are driving innovation and transformation to enable banks to better meet the evolving needs and expectations of their customers in an increasingly digital and interconnected world. Let’s find some latest trends below.

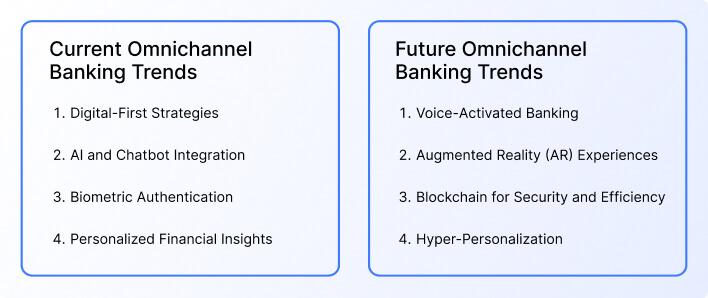

Current Omnichannel Banking Trends

- Digital-First Strategies: Many banks are prioritizing digital channels, offering a seamless online experience and mobile banking applications to cater to the growing demand for convenient and accessible services.

- AI and Chatbot Integration: The integration of artificial intelligence (AI) and chatbots is becoming more prevalent, enhancing customer service by providing instant support, personalized recommendations, and efficient query resolution.

- Biometric Authentication: To bolster security and improve the user experience, biometric authentication methods, such as fingerprint recognition and facial scanning, are being increasingly implemented across various channels.

- Personalized Financial Insights: Banks leverage data analytics to provide customers with personalized financial insights, offering tailored advice, spending patterns analysis, and proactive financial management tools.

Future of Omnichannel Banking Trends

- Voice-Activated Banking: The rise of voice-activated devices is expected to lead to increased integration of voice commands for banking transactions, enabling customers to perform tasks using voice recognition technology.

- Augmented Reality (AR) Experiences: The adoption of augmented reality is anticipated to provide immersive and interactive banking experiences, such as virtual branch visits and enhanced product demonstrations.

- Blockchain for Security and Efficiency: Blockchain technology is expected to be further explored for its potential to enhance security, reduce fraud, and improve the efficiency of transactions across omnichannel platforms.

- Hyper-Personalization: The future of omnichannel banking involves hyper-personalization, where AI-driven algorithms provide highly individualized services, offers, and recommendations based on a customer’s behavior, preferences, and financial goals.

Conclusion

The choice of an omnichannel solution isn’t just a decision; it’s a commitment to revolutionize the way you engage with customers and navigate the technological frontier.

As you select the omnichannel banking solution that aligns with your vision, you’re not just adopting technology; you’re embracing a future where banking is not just a transaction but a journey—a journey that’s seamless, engaging, and thoroughly strategic.

You can start your journey and stay ahead of the competition with REVE Banking Chabot.