In the ever-changing business world, keeping customers around is like holding the golden ticket for long-term success. Two vital metrics that businesses closely monitor to gauge customer loyalty are Churn Rate Vs Retention Rate. These numbers spill the beans on what customers are up to, helping businesses fine-tune their game plans to make sure their fans stick around.

Well, things are more complex than they look. Let’s face it – customers have their own groove. They show up and disappear for a variety of reasons – maybe they found something better, are watching their wallets, or simply decided on a change of pace. You need to do a little number crunching to crack the code on why they’re in and out. Calculate your Churn Rate (how many customers are waving goodbye in a set time) and your Retention Rate (how good you are at making them stick around). It’s like deciphering the steps to the customer dance!

Sounds interesting? it’s time for a deep dive to uncover their secrets!

What is a Churn Rate?

The churn rate, also known as the customer attrition rate, shows the percentage of customers who stop using a service or stop buying from a company in a certain time frame. It’s like a signal that tells us how many customers a business might be losing, giving us clues about any issues the company might be facing.

Achieving zero churn is impossible because it shows how often customers decide not to come back. While every business hopes all customers return, it’s not practical. Over time, having some customers leave, known as a churn rate above zero, is normal. No brand can satisfy everyone.

Monitoring churn is a bit like keeping track of missed chances—stay tuned to this space to find ways to boost repeat business and increase the lifetime value of your customers.

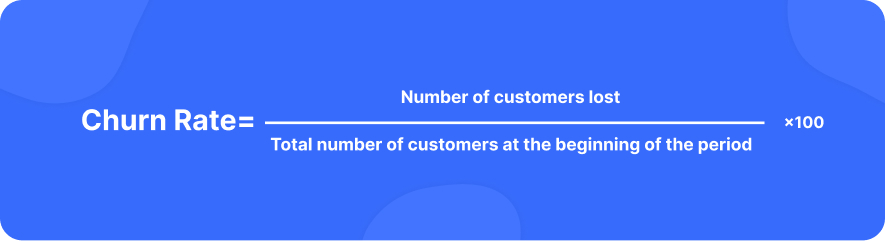

Churn Rate Formula: How to Calculate?

To figure out the churn rate, take the total number of customers who have left, divide it by the number of customers at the beginning of a period, and then multiply by 100.

So how do we calculate the churn rate? Let’s say you had 300 customers at the start of June, and 60 left during the month. In this case, your churn rate would be (60/300) x 100 = 20%.

The Churn Rate Formula at a glance!

What is a Good Churn Rate?

The ideal churn rate varies based on a company’s size and industry. Generally, a lower churn rate is more favorable. Small businesses often view around 5% per month as good, while larger companies aim for even lower rates. Industries with high competition may experience higher churn rates, given customers have more alternatives to explore.

So, what is a good churn rate?

For example, well-established SaaS companies aim for an annual churn rate between 5% and 7%, with a monthly churn of 1% or less – these are seen as acceptable rates. On the flip side, many startups that are still finding their footing in the market might experience higher churn rates. An annual churn averaging 10% to 15% is deemed satisfactory for them.

What is a Retention Rate?

Customer retention is the portion of customers who make repeat purchases within a specific timeframe.

When you calculate the retention rate, you gain insights into how your actions, such as marketing initiatives and internal processes, influence your outcomes, like revenue. A higher retention rate not only reduces the time spent acquiring new customers but also enhances cost-effectiveness. Plus, it can boost profits as customers are more likely to continue investing in a service they like to depend on and trust.

Retention Rate Formula: How to Calculate?

The retention rate formula is pretty simple.

To find your customer retention rate, first, subtract the number of customers who stopped paying at the end of a certain period from the total customers you gained in that time. Then, divide this result by the total number of customers you had at the beginning of the period. Multiply the answer by 100, and there you go – that’s your customer retention rate!

So, how do we calculate the retention rate? Let’s say you started with 100 customers at the beginning of the month, acquired 20 new customers during the month, and ended with 110 customers.

Subtract the number of customers acquired during the month from the total at the end: 110 (end of the month) – 20 (acquired) = 90. Then divide this result by the total number of customers at the start of the period: 90 / 100 = 0.9. Multiply by 100 to get the percentage: 0.9 * 100 = 90%.

So, in this example, the customer retention rate for the month is 90%.

The Retention Rate Formula

What is a Good Customer Retention Rate?

The ideal retention rate comes close to 100%, signaling that a business is keeping almost all of its customers happy. Similar to the churn rate, what’s considered a good retention rate can differ based on the business size and industry. The age of your company matters too. Well-established businesses often boast higher retention rates since they’re already familiar to customers. In contrast, newer companies might see lower rates as more customers try out the service to get to know it better.

The younger SaaS (Software as a Service) companies, for example, tend to have lower retention rates, while more established ones often boast an impressive average retention rate of around 90%.

Churn Rate VS Retention Rate: The Key Differences

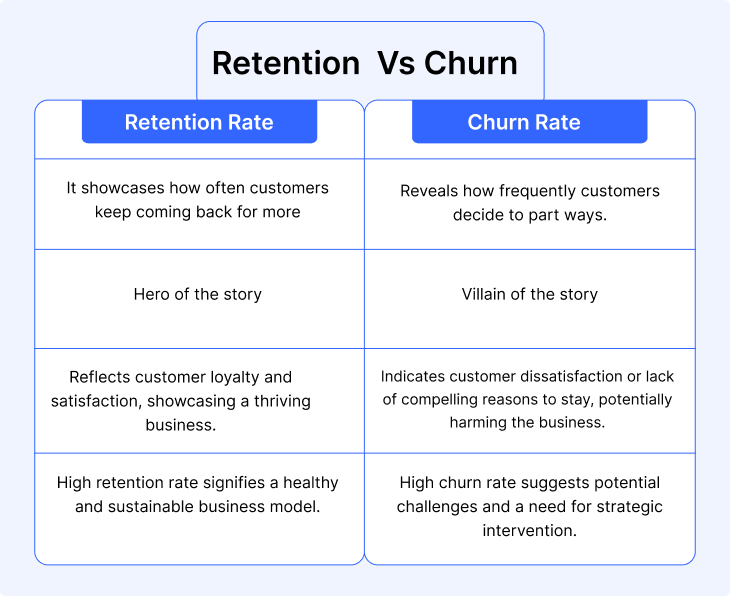

The retention rate and churn rate work hand in hand, each telling a different story about your business.

The retention rate is the hero, showcasing how often customers keep coming back for more. On the other hand, the churn rate is the villain, revealing how frequently customers decide to part ways.

A high retention rate signals a thriving business that attracts repeat customers and builds a reliable brand. When customers return regularly, their lifetime value to the company increases.

In case your churn rate is high, it’s like your business is dealing with a supervillain. Customers might not find a compelling reason to stick around. To tackle this, it’s time to gather customer feedback and create a powerful strategy to keep them hooked.

knowing both rates is the key to writing a successful story. So, whether your business is on the path to superhero success or facing villainous challenges, tracking both rates gives you a comprehensive understanding of your business’s performance.

Why You Should Monitor Churn Rate and Retention Rate?

Running a successful business means understanding the link between churn rate and retention rate. Think of these metrics as your business compass, each revealing a different side of customer behavior. The churn rate shows how many customers leave, while the retention rate focuses on those who stay with you for the long term. Keeping customers is vital for steady growth and profit.

Now, why bother keeping an eye on these rates? Firstly, it’s about maximizing retention. A high retention rate is like a gold star—your business consistently earns and keeps customers happy. When more customers stay than leave, it’s a sign your strategies are working.

Secondly, these metrics are like fortune-telling for your revenue. Knowing your retention and churn rates helps predict future income. It’s not just about meeting current needs; it’s about staying ahead. By staying connected to these metrics, you can foresee revenue gains, allowing you to innovate and stay relevant in the long run. It’s the key to safeguarding your competitive edge in business!

Metrics You Should Look for To Understand Churn and Retention Rate

There are some metrics that you can track to gain a comprehensive understanding of customer behavior, identify areas for improvement, and implement strategies to enhance customer experience and retention. Regularly reviewing and updating these metrics will help ensure ongoing success in managing churn and retention.

When gearing up to create a report on customer retention and churn rates, make sure you’ve got these key metrics on hand:

- How many new customers joined in the past month?

- What about the past year?

- Keep an eye on new customers who cancel after just one month.

- Also, track those who cancel after a year.

- Discover the average time customers stick around before saying goodbye.

So, by closely monitoring metrics such as the number of new customers onboarded, cancellations within the first month and year, or the average customer lifespan, you can gain valuable insights into your business’s churn and retention dynamics.

How to Reduce Churn and Improve Retention: 8 Best Strategies

Now that we’ve got the scoop on the basics, let’s roll up our sleeves and explore some hands-on strategies to reduce the churn rate and supercharge your customer loyalty. While aiming for a zero percent churn is a bit like chasing unicorns – enticing but not always practical – our goal is to find that sweet spot where your business can flourish, and customers stick around for the long haul.

Here are eight power-packed strategies to light your path:

1. Take Different Factors into Account

When figuring out these rates, think about what factors could affect the numbers to understand why they are the way they are. Take into account things like customers who discovered your business through ads or those who found it on their own.

For instance, when examining churn rates, focusing on the segment of customers who regularly engage with your product or service features could provide valuable insights. Customers who actively use and benefit from the core features might exhibit lower churn rates compared to those who haven’t fully explored the product’s capabilities. Considering this variable can guide strategies to emphasize feature adoption, leading to improved retention overall.

2. Motivate Customers

Show your customers some love by offering them perks and reasons to stick around. Shoot them a text or email to keep them in the loop about these great deals and let them know you’re grateful to them for choosing your business. It’s a double win! it’s not just about products or services; it’s about creating a delightful experience that keeps them coming back for more. It’s a fantastic way to build a lasting connection and make both you and your customers happy!

Remember, the effectiveness of incentives often lies in understanding your specific customer base and tailoring the rewards to their preferences and needs. Here are some great ideas for you!

- Savings Offers and Coupon Codes

- Customer Loyalty Programs

- Gifts and Giveaways

- Referral Incentives

- Exclusive Sales Previews

- Subscription Perks

- Customized Appreciation Messages

3. Deliver Excellent Customer Service

Make your business the go-to friend for your customers! Be there when they need you, providing top-notch customer service that’s as quick as a superhero response. Show them their questions, concerns, or even complaints matter by tackling them head-on. If a hiccup happens, don’t hesitate to drop a heartfelt apology and sprinkle in a discount or two to sweeten the deal. Let your customers know they’re not just clients – they’re VIPs shaping the future of your business. It’s not just service; it’s building a friendship that lasts!

There are many customer retention tools available in the market to choose from that can make your life better and let you offer exceptional customer service. Here I would like to recommend REVE Chat, an exceptional AI-powered customer support software. This versatile tool allows you to provide instant assistance on your website, mobile app, and various social media platforms like Facebook, Telegram, Instagram, Viber, and WhatsApp.

With REVE Chat, your support agents can monitor customers in real time, extending personalized assistance proactively—sometimes even before customers ask for it. The AI-powered chatbot takes the reins of your business operations, automating tasks, including customer service, and freeing up your support team to tackle more intricate challenges. Plus, with REVE Chatbot, you can deliver round-the-clock customer service, transcending business hours and busy support agent schedules.

Ready to elevate your customer service game? Dive into a 14-day free trial of REVE Chat, exploring all its unique features. So don’t miss out—SIGN UP today!

4. Gather Input from Customers

Your customers are like treasure, so keeping them smiling is the key to avoid losing them. That’s why it’s super important to check in with them, ask about their experience, and find ways to make it even better! Get the inside scoop from your customers after they make a purchase! Ask them to rate their experience and tell you why they gave that score. This helps you understand both the quality and the feelings behind it, so you can keep them happy and sticking around.

Also, send out timed surveys to measure long-term satisfaction. Find out if they plan to keep using your product and if they’d recommend it to their friends and family. It’s like getting the secret recipe for customer happiness!

So, how can you get customer feedback? Here are some tips for you!

- Questionnaires

- Email invitations

- Social media voting

- Website feedback forms

- In-app feedback

- Client interviews

- Interactions with customer support

- Digital reviews and ratings

- Net Promoter Score (NPS) polls

5. Enhance Your Onboarding Process

Starting with a new product or service can feel like diving into the deep end. If customers can’t easily figure out how to use your product, they might lose interest quickly. To make things smoother, create a simple roadmap or onboarding process. This guides new customers through your product’s features and how everything works.

When customers feel confident using your business, they’re more likely to stick around. Keep a close watch on your onboarding process, fixing any hiccups or obstacles that pop up. It’s all about making sure your customers have a smooth ride!

Some Tips:

- Give customers a friendly and transparent welcome message, outlining what lies ahead.

- Simplify the onboarding process with straightforward, step-by-step tutorials.

- Enhance understanding with visuals and clear instructions for easy follow-through.

- Engage customers with interactive demos, enabling them to explore and practice key features.

- Be ready to assist promptly through chat or support channels throughout onboarding.

- Address common questions and concerns by offering a detailed FAQ section or Help Center.

6. Focus on the Right Kind of Customers

Keeping customers around becomes a breeze when you’ve connected with the perfect audience from the start. A major reason for losing customers is when what you offer isn’t quite right for them.

Craft detailed customer profiles to grasp the ins and outs of your ideal customers’ demographics and buying habits. When you’re in the sales phase, be crystal clear on what the customer aims to achieve, and ensure your product is the perfect match for those goals.

The ideal customers are the ones who not only interact with your products but also fall within your target market, understanding exactly how to make the most of your offerings.

Useful Tips:

- Develop detailed customer profiles encompassing demographic data, preferences, and purchasing habits.

- Take the time during the sales process to understand the goals and challenges of your customers.

- Offer easily understandable and transparent information about your products or services.

- Formulate effective strategies to connect with your target audience, utilizing both online and offline channels.

- Customize your communication approach based on customers’ preferences and past interactions with your brand.

7. Reconnect with Your Users

In the ever-evolving landscape of business, keeping customers happy is key. One standout way to do that? Reconnect with your users! It’s not just about selling stuff—it’s about building a real relationship.

There are many creative and personalized ways to connect with customers, that not only will help you to stop them from leaving, but you’ll also build long-lasting relationships that go beyond just buying and selling.

Here are some ideas for you!

- Get personal with your messages! Whether it’s an email, newsletter, or social media post, make customers feel like you know what they want.

- Share the love—encourage them to spill their thoughts and opinions.

- Show some appreciation for their loyalty with cool rewards like discounts or exclusive perks to keep them hanging out with your brand.

- Keep things exciting by throwing in surprises, like personalized offers to make their day.

- Stay on top of things by tackling customer concerns before they become big problems, proving that you’ve got their back.

- Join the party on social media—respond to comments, ask for their thoughts, and build a tight-knit community around your brand.

- And, hey, why not make their experience even better? Hook them up with helpful resources or guides that add a little extra magic to your product or service!

8. Transit Customers to Yearly Contracts

Imagine this scenario: What if you made things extra special for your existing customers, enticing them with discounts or thrilling incentives to transition to annual contracts? It’s like turning a one-time date into a long-term relationship. Once they make that commitment, the chances of them drifting away become lower. It’s a mutually beneficial arrangement – they enjoy added perks, and you establish a more steadfast bond with your customers. So, why not infuse a touch of annual contract magic and witness a significant drop in those churn rates? It’s a recipe for success!

What to offer to see the magic? Here are some ideas for you.

- Special Discounts

- Extra Incentives

- Adaptable Payment Options

- Complimentary Trials

- Tailored Packages

- Add-On Flexibilities

- Limited Offers

- Opportunities to Upgrade

- Referral Rewards

Assessing Your Performance!

Now that you’ve got the basics of Churn Rate Vs Retention Rate, let’s see how you’re doing. Are you keeping up with or beating the industry averages?

Work with your marketing and sales team closely to cook up a plan that’s all about data and boosting your retention while kicking churn to the curb. The secret sauce? Keep your customers happy.

Here’s one last tip: Look for different strategies, focus on satisfaction, and watch your retention climb and churn drop – all while supercharging your customer lifetime value!

To know more about customer lifetime value, you can check our latest blog on CLV Vs LTV (Customer Lifetime Value Vs Lifetime Value).