The cost of sales is a fundamental aspect of financial analysis and strategic planning for businesses of all types and sizes. It’s calculated to measure how much is being spent to produce a sellable good. When a company has an accurate number of the cost of sales, it can easily make informed decisions in various aspects, be it determining the budget, taxes, and overall financial well-being of the company.

The cost of sales is always a key component, whether a company wants to calculate the gross profit or wants to know the operating expenses. More importantly, businesses need to calculate the COS to set the right pricing strategies to avoid under or over-pricing. This calculation is essential in various other aspects as well, such as inventory management, financial reporting, cost control, and taxation.

In this blog, we will explore the cost of sales in detail, understand its definition, importance, formula, and how to calculate it.

But first, let’s get started with understanding what exactly is cost of sales…

What is the Cost of Sales?

Cost of sales represents the total direct expenses associated with producing a product or service sold to customers. It also includes the expenses related to purchasing the goods or services that a business needs for a specific accounting period. So, in essence, it’s the overall cost incurred to acquire, manufacture, and deliver the products or services to the end customers.

For businesses, the cost of sales is a key accounting concept that is used to calculate the gross profit after subtracting the expenses in delivering the products. This cost is closely related to product costs because both have many similar elements. However, there is a key difference between the two concepts – product cost is considered inventory while the cost of sales is part of the income statement.

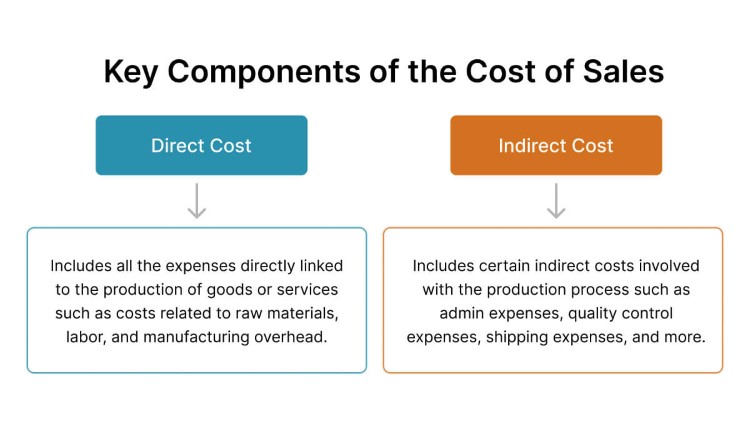

Key Components of the Cost of Sales

The cost of sales is a key concept in accounting that helps businesses determine the profit based on the expenditure in producing and delivering products to customers. It consists of two key components, including –

- Direct Costs – As the name suggests, these costs include all the expenses directly linked to the production of goods or services. They include costs related to raw materials, labor, and manufacturing overhead.

- Indirect Costs – Sometimes, certain indirect costs may also be involved with the production process and that’s why they are added to the cost of sales. These costs may include admin expenses, quality control expenses, shipping expenses, and more.

What to Include in Cost of Sales Calculation?

It’s true that expense management is a complex task. Account people often feel confused about what expenses to include in the cost of sales calculation and what to leave out. While making this decision, the key consideration should be to include every expense that was paid to manufacture the goods or deliver the service. If a specific expense causes the production to stop, then naturally, it should always be included in the cost of sales calculation.

Here is a list of all the costs to be included –

- All the costs that are directly tied to manufacturing or selling products

- Direct labor and material costs

- Software licensing

- Cost of packaging for products

- Cost of storing products or materials

- Wages that were paid for direct involvement with the manufacture or delivery of goods and services

- Expenses on the salesperson responsible for selling the products

What Not to Include in Cost of Sales Calculation?

Every business is unique, so the decision of what to include and what not in the cost of sales calculation is never a standard one. All the inclusions and exclusions depend entirely on the type of business and the type of products being manufactured. In general, however, the following things are not included in the cost of sales calculations –

- All the expenses that are not involved in production either directly or indirectly

- Expenses related to up-selling

- Commissions paid to the salespeople

- Expsesens in the sales and marketing department

- Cost of specific overheads

- Cost of product development

Cost of Sales Formula

The formula to calculate the cost of sales is –

Cost of Sales = Opening Inventory + Purchases (or production costs) – Closing Inventory

In this formula, opening inventory is the total value of stock that a company has at the start of the accounting period and it may also include the cost of goods unsold from the previous account period.

Purchases or production costs refer to the cost of acquiring or producing additional inventory. It includes various costs such as those related to the raw material, labor, and anything incurred on procurement or in manufacturing.

Closing inventory refers to the total value of merchandise at the end and may also include the cost of goods still in stock or not sold.

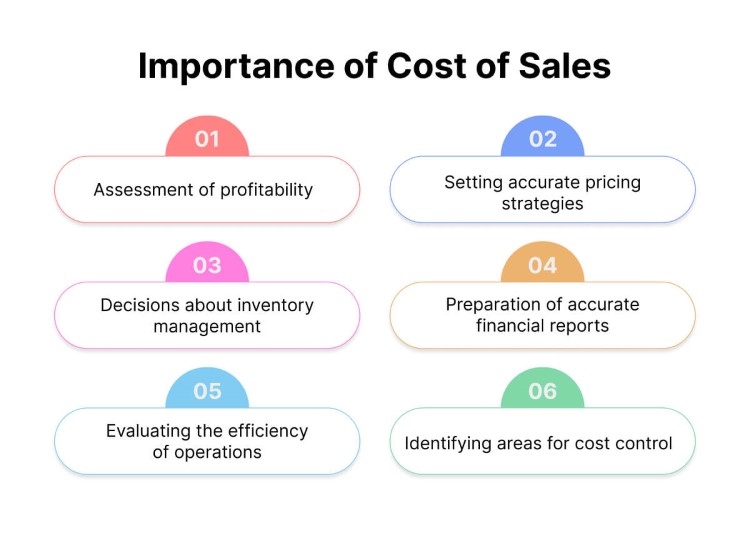

Importance of Cost of Sales

For businesses, cost of sales (COS) is a vital financial metric as it gives detailed info into various aspects of the operations. You can rely on this metric to make informed decisions and achieve financial success for the business. More so, its use can help in assessing many things, including profit, price, inventory, and so on.

Here are the reasons behind the importance of COS –

- Assessment of profitability – Profit is assessed based on the revenue that is left after accounting for the costs associated with producing or procuring goods or services. That’s why the cost of sales becomes a critical indicator of a company’s profitability. It can also tell how efficiently a company is converting revenue into profit.

- Setting accurate pricing strategies – A business may fail to set an appropriate pricing strategy if it lacks the cost of sales knowledge. When there is no clear understanding of the COS, a business might set prices that are either too low or too high, resulting in a lack of competitiveness.

[

- Decisions about inventory management – Cost of sales calculation is essential for a business to track and monitor the value of inventory at the start and end of the accounting period. This calculation is also vital in making robust decisions about stock levels, orders, and inventory replenishments.

- Preparation of accurate financial reports – The cost of sales is a vital component of financial statements. It’s key to creating an income statement and giving a comprehensive view of the revenue and expenses of the organization. Without COS information, a business might fail to comply with accounting standards, leading to mistrust with key stakeholders.

- Evaluating the efficiency of operations – Gross profit margin is often assessed by comparing COS to revenue. A higher profit indicates that a company is managing its direct costs well whereas a lower margin shows a need for improvement.

- Identifying areas for cost control – A business is better able to implement cost control measures when it has a cost of sales calculation. The COS information proves beneficial in identifying ways to minimize various production costs and increase profitability.

How to Calculate Cost of Sales?

We already know the simple cost of sales formula that can be used to calculate the total cost of sales.

For example, let’s suppose a company has $30,000 of inventory on hand at the start of the month. It then further spends around $10,000 on wages, raw materials, and delivery. With $ 18,000 worth of inventory at the end of the month, the company can use the cost of sales formula to calculate the cost of sales during the month.

As we know –

Cost of Sales = Beginning Inventory + Purchases – Ending Inventory

So,

Cost of Sales = $30,000 + $ 10,000 – $18,000 = $22,000

However, a company needs to have the following data on hand to calculate the total cost of sales –

- Determine the total direct materials used in the production of items for sale

- Total costs to purchase products for resales

- Calculate all direct labor expenses paid to the people directly responsible for selling products

- Track all sales figures during the specified accounting period for accurate financial reporting

- Calculate net sales

- Compare the cost of sales to net sales

Is Cost of Sales the Same as Cost of Goods Sold?

Many people confuse whether the cost of sales (COS) and the cost of goods sold (COGS) are two entirely different concepts.

Well, they should know that both are essentially the same thing and are often used interchangeably. Both mean the same thing as they refer to the direct costs linked with producing or purchasing the goods or services that a company produces or sells during a specific accounting period.

Both include various costs like expenses for raw materials, labor, and manufacturing overhead, and both include any other costs that are directly part of the production of the products sold by the company.

When we talk about the cost of sales and the cost of goods sold, we see the use of different terminology across industries and regions but the underlying concept is the same. Both are key components in calculating a company’s gross profit. Both are part of the income statement and serve as key metrics for evaluating the profit and operational efficiency of a business.

Different Accounting Methods for COGS

Several accounting methods exist when it comes to calculating the cost of goods sold. The method a company decides to use can have a big impact on its financial statement and tax liability. More so, the value of the COGS will depend on the inventory costing method adopted by a company. FIFO, LIFO, and the average cost method are the most adopted methods.

There are several accounting methods for calculating the cost of goods sold (COGS), and the method a company uses can significantly impact its financial statements and tax liability. Here are some of the primary accounting methods for COGS:

FIFO (First-In, First-Out)

In this method, the items that are sold first are assumed to be the first items added to the inventory. So, the cost of the oldest inventory is considered first in this method when COGS is calculated. The purpose of using FIFO is to obviously get a more accurate idea of the current cost of goods sold but it might lead to higher taxable income when inflation is more.

LIFO (Last-In, First-Out)

In this method, the most recently procured items are assumed to be the first ones sold. So, it’s obvious that the cost of the most recent inventory items is used when calculating COGS. This method may result in a lower taxable income during inflationary times but might not fail to accurately show the current cost of goods sold.

Weighted Average

It’s a simple method and best suited for situations where inventory items are similar and hard to track individually. In this method, the average cost of all units is calculated first and then this cost helps determine COGS.

Specific Identification

This method is used when each item in the inventory is easy to identify with the actual cost of each item tracked easily. This method is suitable for high-value inventory items and it also gives the most accurate picture of COGS.

Final Thoughts

The cost of sales is the direct cost of producing a good and it includes all the expenses of the materials and labor used in producing the good. It’s a key metric that has a direct impact on a company’s profit. For businesses, it’s important to manage their COS to achieve higher profits. If your company is able to reduce COGS through more production process efficiency, it can surely become more profitable.